Income can be an important part of an investment’s return, but it is not the whole picture. A high yield may look attractive on its own, while the full result also depends on price movement, fees, taxes, and portfolio weight.

Yield is only one input

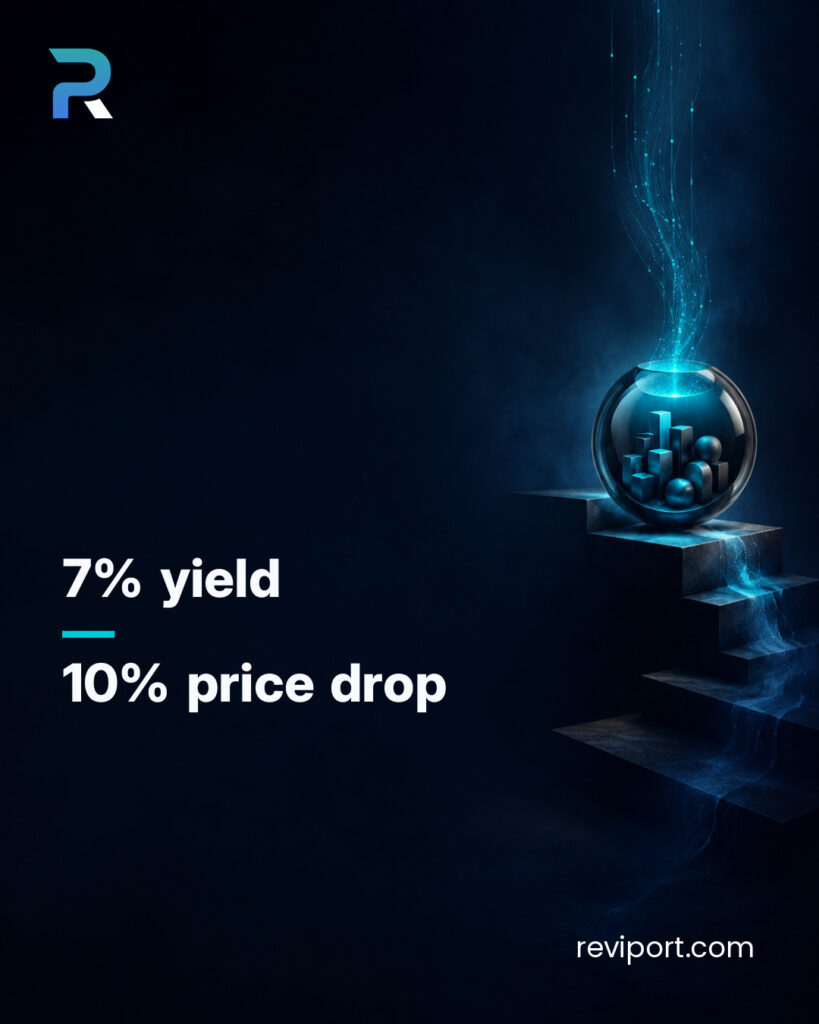

Yield usually describes income compared with the price of an investment. For example, a holding worth €1,000 that pays €70 over a year has a 7% yield before considering other factors.

That number can be useful, but it does not automatically show whether the overall position gained or lost value.

A simple hypothetical example

Imagine a holding starts the year at €1,000. It pays €70 in income during the year, but its price falls by €100.

In that simplified example, the income helped, but the total result before fees or taxes is still negative:

- Income received: +€70

- Price movement: -€100

- Net change before fees or taxes: -€30

This does not mean income-focused investments are bad. It means yield needs context. A portfolio review should consider both income and price movement rather than treating the income number alone as the full story.

Why portfolio weight matters

The same yield can matter differently depending on position size. A 7% yield on a small holding may have limited impact on the full portfolio. A 7% yield on a large holding can shape more of the portfolio’s return and risk experience.

That is why investors often benefit from looking beyond the headline yield and asking how much of the portfolio depends on that holding, asset class, or income source.

Useful review questions

- How much of the return came from income?

- How much came from price movement?

- How large is the position inside the full portfolio?

- Does the income source depend on one sector, asset type, or theme?

Reviport is designed to help investors view holdings in portfolio context, so an income number can be considered alongside allocation, position size, and overall exposure.